Asked by Claudia Gonzalez on Jul 13, 2024

Verified

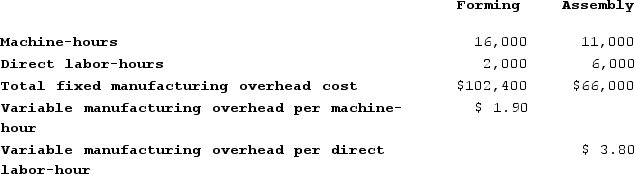

Amason Corporation has two production departments, Forming and Assembly. The company uses a job-order costing system and computes a predetermined overhead rate in each production department. The Forming Department's predetermined overhead rate is based on machine-hours and the Assembly Department's predetermined overhead rate is based on direct labor-hours. At the beginning of the current year, the company had made the following estimates:

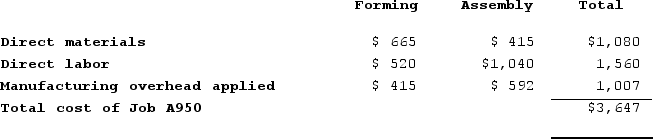

During the current month the company started and finished Job A950. The following data were recorded for this job:

During the current month the company started and finished Job A950. The following data were recorded for this job:

Required:Calculate the selling price for Job A950 if the company marks up its unit product costs by 30% to determine selling prices.

Required:Calculate the selling price for Job A950 if the company marks up its unit product costs by 30% to determine selling prices.

Predetermined Overhead Rate

An estimated rate used to allocate manufacturing overhead to products or job orders based on a certain activity base.

Machine-Hours

A measure of the amount of time a machine is operated within a specific period, often used for allocating machine costs to products.

Direct Labor-Hours

Total labor hours of workers directly engaged in the production line.

- Calculate the market costs of jobs by implementing markups on the expenses of production.

Verified Answer

Overhead applied to Job A950

Learning Objectives

- Calculate the market costs of jobs by implementing markups on the expenses of production.

Related questions

Hultquist Corporation Has Two Manufacturing Departments--Forming and Customizing ...

Hultquist Corporation Has Two Manufacturing Departments--Forming and Customizing ...

Vasilopoulos Corporation Has Two Production Departments, Casting and Assembly ...

Dancel Corporation Has Two Production Departments, Milling and Finishing ...

Lotz Corporation Has Two Manufacturing Departments--Casting and Finishing ...