Asked by Michael Byars on Jun 18, 2024

Verified

Which of the following statements concerning the unit product cost of Product W2 is true?

A) The unit product cost of Product W2 under traditional costing is less than its unit product cost under activity-based costing by $209.06.

B) The unit product cost of Product W2 under traditional costing is greater than its unit product under activity-based costing by $12.41.

C) The unit product cost of Product W2 under traditional costing is greater than its unit product under activity-based costing by $209.06.

D) The unit product cost of Product W2 under traditional costing is less than its unit product cost under activity-based costing by $12.41.

Unit Product Cost

Unit product cost is the total cost (including materials, labor, and overhead) divided by the total number of units produced, representing the cost per unit.

Activity-Based Costing

A costing methodology that assigns overhead and indirect costs to specific activities, providing more accurate product costing.

- Gain an understanding of the core principles of activity-based costing while identifying the differences between traditional costing approaches and ABC.

- Examine the influence of different costing approaches on product cost determination.

Verified Answer

SG

Shruthi GurumurthiJun 25, 2024

Final Answer :

D

Explanation :

Predetermined overhead rate = Estimated total overhead ÷ Total direct labor-hours

= $501,744 ÷ 4,800 DLHs = $104.53 per DLH (rounded)

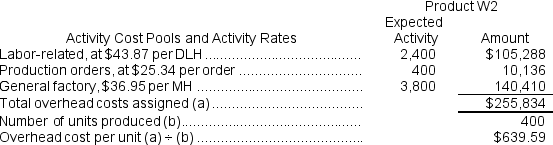

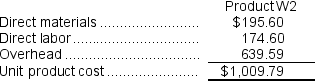

Computation of traditional unit product cost: Computation of activity rates:

Computation of activity rates:  Computation of the overhead cost per unit under activity-based costing.

Computation of the overhead cost per unit under activity-based costing.  Computation of unit product cost under activity-based costing.

Computation of unit product cost under activity-based costing.  The difference in unit product costs is:

The difference in unit product costs is:  The unit product cost of Product W2 under traditional costing is less than its unit product cost under activity-based costing by $12.41.

The unit product cost of Product W2 under traditional costing is less than its unit product cost under activity-based costing by $12.41.

Reference: CH04-Ref26

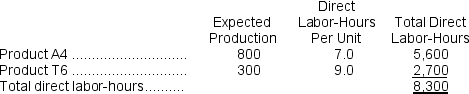

Kroll, Inc., manufactures and sells two products: Product A4 and Product T6.Data concerning the expected production of each product and the expected total direct labor-hours (DLHs)required to produce that output appear below: The direct labor rate is $21.50 per DLH.The direct materials cost per unit is $212.40 for Product A4 and $295.50 for Product T6.

The direct labor rate is $21.50 per DLH.The direct materials cost per unit is $212.40 for Product A4 and $295.50 for Product T6.

The company is considering adopting an activity-based costing system with the following activity cost pools, activity measures, and expected activity:

= $501,744 ÷ 4,800 DLHs = $104.53 per DLH (rounded)

Computation of traditional unit product cost:

Computation of activity rates: Computation of the overhead cost per unit under activity-based costing. Computation of unit product cost under activity-based costing. The difference in unit product costs is: The unit product cost of Product W2 under traditional costing is less than its unit product cost under activity-based costing by $12.41.Reference: CH04-Ref26

Kroll, Inc., manufactures and sells two products: Product A4 and Product T6.Data concerning the expected production of each product and the expected total direct labor-hours (DLHs)required to produce that output appear below:

The direct labor rate is $21.50 per DLH.The direct materials cost per unit is $212.40 for Product A4 and $295.50 for Product T6.The company is considering adopting an activity-based costing system with the following activity cost pools, activity measures, and expected activity:

Learning Objectives

- Gain an understanding of the core principles of activity-based costing while identifying the differences between traditional costing approaches and ABC.

- Examine the influence of different costing approaches on product cost determination.

Related questions

Which of the Following Statements Concerning the Unit Product Cost ...

Faiella, Inc ...

Adelberg Corporation Makes Two Products: Product a and Product B ...

Figge and Mathews Public Limited Company, a Consulting Firm, Uses ...

Desjarlais Corporation Uses the Following Activity Rates from Its Activity-Based ...