Asked by Helmut Andres Florencia Roldan on May 20, 2024

Verified

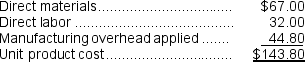

Mcniff Corporation makes a range of products.The company's predetermined overhead rate is $28 per direct labor-hour, which was calculated using the following budgeted data:  Management is considering a special order for 200 units of product O96S at $122 each.The normal selling price of product O96S is $149 and the unit product cost is determined as follows:

Management is considering a special order for 200 units of product O96S at $122 each.The normal selling price of product O96S is $149 and the unit product cost is determined as follows:  If the special order were accepted, normal sales of this and other products would not be affected.The company has ample excess capacity to produce the additional units.Assume that direct labor is a variable cost, variable manufacturing overhead is really driven by direct labor-hours, and total fixed manufacturing overhead would not be affected by the special order.

If the special order were accepted, normal sales of this and other products would not be affected.The company has ample excess capacity to produce the additional units.Assume that direct labor is a variable cost, variable manufacturing overhead is really driven by direct labor-hours, and total fixed manufacturing overhead would not be affected by the special order.

Required:

The financial advantage (disadvantage)for the company as a result of accepting this special order would be:

Predetermined Overhead Rate

An established rate used to assign overhead costs to products or job orders, calculated in advance based on anticipated costs and activities.

Special Order

An order typically outside the company's normal production that has unique requirements and pricing.

Excess Capacity

A situation where a company can produce more than is needed to meet the demand, often resulting in idle resources or underused assets.

- Scrutinize unique orders to determine their economic ramifications.

Verified Answer

DS

Dorreen San PedroMay 22, 2024

Final Answer :

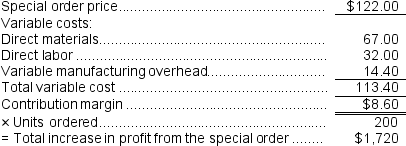

Direct materials, direct labor, and variable manufacturing overhead are relevant in this decision.Fixed manufacturing overhead is not relevant because it would not be affected by the decision.The variable portion of the manufacturing overhead rate is computed as follows:  The direct-labor hours per unit for the special order can be determined as follows:

The direct-labor hours per unit for the special order can be determined as follows:  Consequently, the variable manufacturing overhead for the special order would be:

Consequently, the variable manufacturing overhead for the special order would be:  Putting this all together:

Putting this all together:

The direct-labor hours per unit for the special order can be determined as follows: Consequently, the variable manufacturing overhead for the special order would be: Putting this all together:

Learning Objectives

- Scrutinize unique orders to determine their economic ramifications.