Asked by Murali Krishna on Apr 27, 2024

Verified

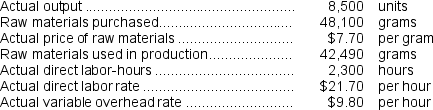

The variable overhead efficiency variance for October is:

A) $1,400 Favorable

B) $1,225 Unfavorable

C) $1,900 Unfavorable

D) $2,700 Favorable

Variable Overhead Efficiency Variance

The difference between actual and budgeted variable overhead costs, attributable to differences in productive efficiency.

Favorable

A term used in finance and accounting to describe a situation or variance that is better than expected or budgeted, often indicating profits or gains.

- Obtain knowledge on the intricacies and computation of variable overhead rate and efficiency variances.

Verified Answer

TH

Tahir HussainApr 28, 2024

Final Answer :

B

Explanation :

The variable overhead efficiency variance is calculated as (actual hours - standard hours) x standard rate. Substituting the given values, we get ($39,000/6,000 hours - 4 hours per unit) x $5 per hour = $1,225 unfavorable.

Explanation :

SH = 3,750 units × 1.4 hours per unit = 5,250 hours

Variable overhead efficiency variance = (AH − SH)× SR

= (5,600 hours − 5,250 hours)× $3.50 per hour

= (350 hours)× $3.50 per hour

= $1,225 U

Reference: CH09-Ref45

Pippin Inc.has provided the following data concerning one of the products in its standard cost system.Variable manufacturing overhead is applied to products on the basis of direct labor-hours. The company has reported the following actual results for the product for June:

The company has reported the following actual results for the product for June:

Variable overhead efficiency variance = (AH − SH)× SR

= (5,600 hours − 5,250 hours)× $3.50 per hour

= (350 hours)× $3.50 per hour

= $1,225 U

Reference: CH09-Ref45

Pippin Inc.has provided the following data concerning one of the products in its standard cost system.Variable manufacturing overhead is applied to products on the basis of direct labor-hours.

The company has reported the following actual results for the product for June:

Learning Objectives

- Obtain knowledge on the intricacies and computation of variable overhead rate and efficiency variances.