Asked by Alexis Shyanne on Apr 29, 2024

Verified

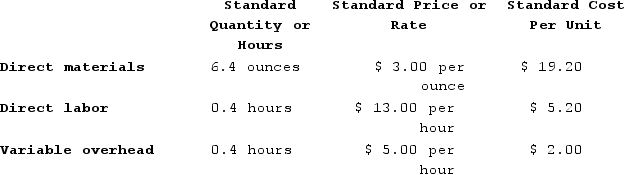

Majer Corporation makes a product with the following standard costs:  The company reported the following results concerning this product in February.

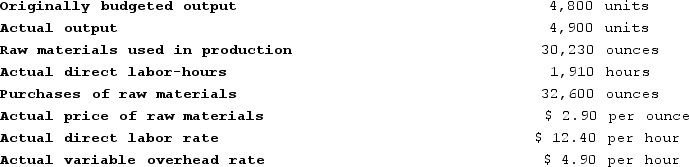

The company reported the following results concerning this product in February.

The company applies variable overhead on the basis of direct labor-hours. The direct materials purchases variance is computed when the materials are purchased.The variable overhead efficiency variance for February is:

The company applies variable overhead on the basis of direct labor-hours. The direct materials purchases variance is computed when the materials are purchased.The variable overhead efficiency variance for February is:

A) $245 Unfavorable

B) $245 Favorable

C) $250 Favorable

D) $250 Unfavorable

Variable Overhead Efficiency Variance

A measure used to assess the efficiency of variable overhead resource usage, calculated as the difference between actual and expected costs based on standard usage rates.

Direct Materials Purchases Variance

The difference between the actual cost of materials purchased and the expected cost at standard prices.

Direct Labor-Hours

An alternative term for direct labor-hour, referring to the labor time spent by employees directly on manufacturing a product.

- Ascertain and evaluate the differences in variable manufacturing overhead, including analysis of rate and efficiency variances.

Verified Answer

Variable overhead rate = $7.50 per direct labor hour

Actual direct labor hours = 1,600 hours

Standard hours allowed = 800 units x 2 direct labor hours per unit = 1,600 hours

Variable overhead efficiency variance = (actual hours - standard hours) x variable overhead rate

= (1,600 - 1,600) x $7.50

= $0

Since the actual hours worked are equal to the standard hours allowed, the variable overhead efficiency variance is $0, or $250 favorable. However, since there is no option for $0, we choose the closest favorable amount, which is $250.

Learning Objectives

- Ascertain and evaluate the differences in variable manufacturing overhead, including analysis of rate and efficiency variances.

Related questions

Puvo, Incorporated, Manufactures a Single Product in Which Variable Manufacturing ...

Majer Corporation Makes a Product with the Following Standard Costs ...

If Variable Manufacturing Overhead Is Applied on the Basis of ...

The Following Standards for Variable Manufacturing Overhead Have Been Established ...

The Unitization of Fixed Overhead Costs Is Useful from a ...