Asked by Heather Hernandez on Jun 15, 2024

Verified

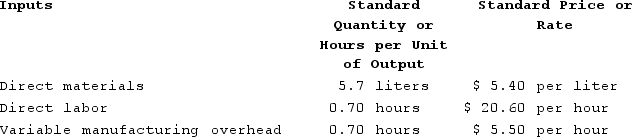

Fluegge Incorporated has provided the following data concerning one of the products in its standard cost system. Variable manufacturing overhead is applied to products on the basis of direct labor-hours.  The company has reported the following actual results for the product for December:

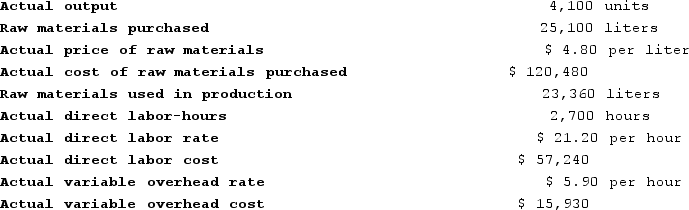

The company has reported the following actual results for the product for December:

The labor efficiency variance for the month is closest to:

The labor efficiency variance for the month is closest to:

A) $3,604 Unfavorable

B) $3,604 Favorable

C) $3,502 Favorable

D) $3,502 Unfavorable

Manufacturing Overhead

All indirect costs associated with manufacturing, such as indirect materials, indirect labor, and other overhead costs.

Labor Efficiency Variance

The difference between the actual labor hours used and the standard labor hours expected, multiplied by the standard labor rate.

- Carry out the computation and examination of efficiency and rate differences in direct labor.

Verified Answer

FK

Faisal KassabJun 22, 2024

Final Answer :

C

Explanation :

To calculate the labor efficiency variance, we need to compare the actual direct labor hours worked with the standard direct labor hours allowed for the actual output.

Actual direct labor hours = 6,300

Standard direct labor hours allowed = 7,700 (11,000 units x 0.7 DLH per unit)

So, the labor efficiency variance = (standard hours allowed - actual hours) x standard rate per hour

= (7,700 - 6,300) x $0.45

= $630 x $0.45

= $283.50 favorable

Therefore, the closest option is C) $3,502 Favorable.

Actual direct labor hours = 6,300

Standard direct labor hours allowed = 7,700 (11,000 units x 0.7 DLH per unit)

So, the labor efficiency variance = (standard hours allowed - actual hours) x standard rate per hour

= (7,700 - 6,300) x $0.45

= $630 x $0.45

= $283.50 favorable

Therefore, the closest option is C) $3,502 Favorable.

Learning Objectives

- Carry out the computation and examination of efficiency and rate differences in direct labor.

Related questions

Milar Corporation Makes a Product with the Following Standard Costs ...

Hofbauer Incorporated Has Provided the Following Data Concerning One of ...

Chhom Corporation Makes a Product Whose Direct Labor Standards Are ...

Wolery Incorporated Has Provided the Following Data Concerning One of ...

The Following Labor Standards Have Been Established for a Particular ...