Asked by Jocelyn Calderon on Jul 03, 2024

Verified

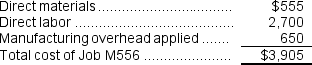

Cardosa Corporation uses a job-order costing system with a single plantwide predetermined overhead rate based on machine-hours.The company based its predetermined overhead rate for the current year on 70,000 machine-hours, total fixed manufacturing overhead cost of $308,000, and a variable manufacturing overhead rate of $2.10 per machine-hour.Job M556, which was for 50 units of a custom product, was recently completed.The job cost sheet for the job contained the following data:  Required:

Required:

a.Calculate the total job cost for Job M556.

b.Calculate the unit product cost for Job M556.

Machine-Hours

A measure of production volume or activity based on the number of hours machines are operated within a specified period.

Predetermined Overhead Rate

A rate used to allocate manufacturing overhead costs to products or job orders, calculated before the period begins based on estimates.

- Assess the full cost of a job by the application of job-order costing principles.

- Ascertain the cost associated with each unit for selected jobs.

Verified Answer

MJ

Megan JohnsonJul 09, 2024

Final Answer :

a.Estimated total manufacturing overhead cost = Estimated total fixed manufacturing overhead cost + (Estimated variable overhead cost per unit of the allocation base × Estimated total amount of the allocation base)= $308,000 + ($2.10 per machine-hour × 70,000 machine-hours)= $308,000 + $147,000 = $455,000

Predetermined overhead rate = Estimated total manufacturing overhead cost ÷ Estimated total amount of the allocation base = $455,000 ÷ 70,000 machine-hours = $6.50 per machine-hour

Overhead applied to a particular job = Predetermined overhead rate x Amount of the allocation base incurred by the job = $6.50 per machine-hour × 100 machine-hours = $650

Predetermined overhead rate = Estimated total manufacturing overhead cost ÷ Estimated total amount of the allocation base = $455,000 ÷ 70,000 machine-hours = $6.50 per machine-hour

Overhead applied to a particular job = Predetermined overhead rate x Amount of the allocation base incurred by the job = $6.50 per machine-hour × 100 machine-hours = $650

Learning Objectives

- Assess the full cost of a job by the application of job-order costing principles.

- Ascertain the cost associated with each unit for selected jobs.

Related questions

The Unit Product Cost for Job A496 Is Closest To

Dancel Corporation Has Two Production Departments, Milling and Finishing ...

Teasley Corporation Uses a Job-Order Costing System with a Single ...

The Unit Product Cost for Job K818 Is Closest To

Garner Company Begins Operations on July 1 2017 \quad \(\quad ...