Asked by Siqian Chang on May 21, 2024

Verified

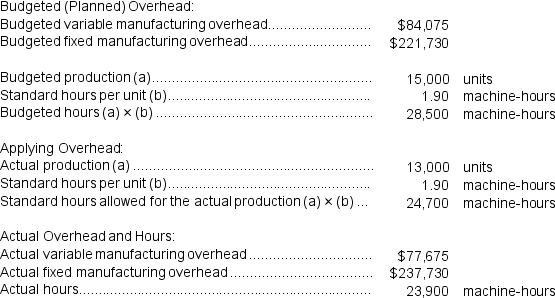

Berk Incorporated makes a single product--a critical part used in commercial airline seats.The company has a standard cost system in which it applies overhead to this product based on the standard machine-hours allowed for the actual output of the period.Data concerning the most recent year appear below:  Required:

Required:

a.Compute the variable component of the company's predetermined overhead rate.

b.Compute the fixed component of the company's predetermined overhead rate.

c.Determine the variable overhead rate variance for the year.

d.Determine the variable overhead efficiency variance for the year.

e.Determine the fixed overhead budget variance for the year.

f.Determine the fixed overhead volume variance for the year.

Predetermined Overhead Rate

A rate used to allocate manufacturing overhead cost to products or job orders, based on expected overhead costs and a chosen allocation base.

Variable Component

A variable component refers to a part of a cost or expense that varies directly with the level of output or activity.

Fixed Component

A portion of total costs that remains constant, regardless of changes in the production level or sales volume.

- Comprehend the computation of variable and fixed elements in the predetermined overhead rate.

- Compute the variance in variable overhead rate and the discrepancies in efficiency.

- Determine the discrepancies in budgeted and actual volumes for fixed overhead.

Verified Answer

= $2.95 per machine-hour

b.Fixed component of the predetermined overhead rate = $221,730/28,500 machine-hours

= $7.78 per machine-hour

c.Variable overhead rate variance = (AH × AR)- (AH × SR)

= ($77,675)- (23,900 machine-hours × $2.95 per machine-hour)

= ($77,675)- ($70,505)

= $7,170 U

d.Variable overhead efficiency variance = (AH - SH)× SR

= (23,900 machine-hours - 24,700 machine-hours)× $2.95 per machine-hour

= (-800 machine-hours)× $2.95 per machine-hour

= $2,360 F

e.Budget variance = Actual fixed overhead - Budgeted fixed overhead

= $237,730 - $221,730 = $16,000 U

f.Volume variance = Budgeted fixed overhead - Fixed overhead applied to work in process

= $221,730 - ($7.78 per machine-hour × 24,700 machine-hours)

= $221,730 - ($192,166)

= $29,564 U

or

Volume variance = Fixed component of the predetermined overhead rate x (Denominator hours - Standard hours allowed for the actual output)

= $7.78 per machine-hour x (28,500 machine-hours - 24,700 machine-hours)

= $7.78 per machine-hour x (28,500 machine-hours - 24,700 machine-hours)

= $7.78 per machine-hour x (3,800 hours)

= $29,564 U

Learning Objectives

- Comprehend the computation of variable and fixed elements in the predetermined overhead rate.

- Compute the variance in variable overhead rate and the discrepancies in efficiency.

- Determine the discrepancies in budgeted and actual volumes for fixed overhead.

Related questions

Fenderson Incorporated Makes a Single Product--A Cooling Coil Used in ...

Pearlman Incorporated Makes a Single Product--An Electrical Motor Used in ...

Moozi Dairy Products Processes and Sells Two Products: Milk and ...

Edlow Incorporated Makes a Single Product--A Critical Part Used in ...

The Variable Overhead Efficiency Variance for the Month Is Closest ...