Asked by Brianna Villella on Jun 15, 2024

Verified

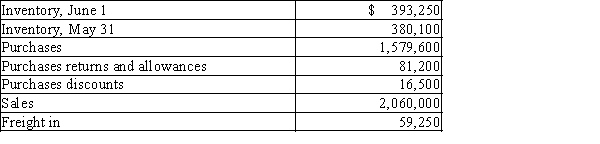

Using the following data taken from Payton Inc., which uses a periodic inventory system, determine the gross profit to be reported on the income statement for the year ended May 31.

Periodic Inventory System

An inventory accounting system where stock levels are updated at regular intervals, not continuously.

Gross Profit

Gross profit is the difference between sales revenue and the cost of goods sold, indicating how efficiently a company is producing or sourcing its products.

Income Statement

A financial statement that reports a company's financial performance over a specific accounting period, showing revenue, expenses, and net income.

- Evaluate gross profit and develop matching sections of the income statement.

Verified Answer

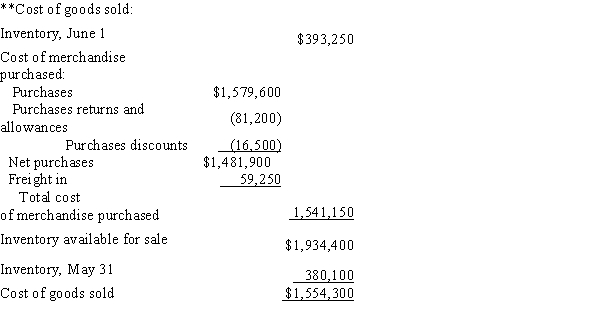

*Cost of goods sold

(81,200)

(81,200)

Learning Objectives

- Evaluate gross profit and develop matching sections of the income statement.

Related questions

During the Current Year, Merchandise Is Sold for $147,500 Cash ...

The Following Data Were Extracted from the Accounting Records of ...

Chen Company's Financial Information Is Presented Below The Missing Amounts ...

Gross Profit Does Not Appear ...

Complete the Following Data Taken from the Condensed Income Statements ...