Asked by Margaret Everett on May 01, 2024

Verified

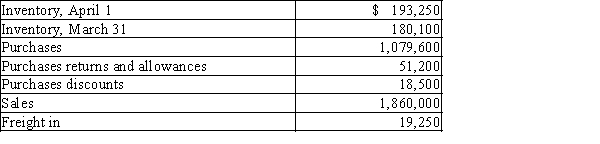

Using the following data taken from Hsu's Imports Inc. which uses a periodic inventory system, determine the gross profit to be reported on the income statement for the year ended March 31.

Periodic Inventory System

An inventory accounting system where updates to inventory levels are made periodically, typically at the end of an accounting period, rather than after each transaction.

Gross Profit

The difference between sales revenue and the cost of goods sold before deducting operating expenses, interest, and taxes.

Income Statement

A financial statement that shows a company's revenues and expenses over a specific period, culminating in the net income or loss for that period.

- Accurately compute the gross profit.

Verified Answer

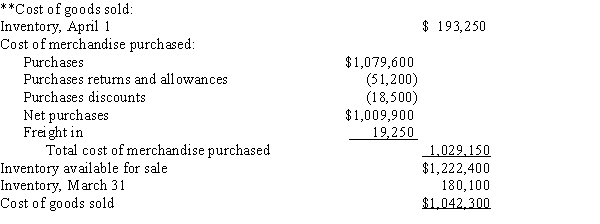

*Cost of goods sold

Learning Objectives

- Accurately compute the gross profit.

Related questions

Calculate the Gross Profit for Jonas Company Based on the ...

During the Current Year, Merchandise Is Sold for $117,500 Cash ...

During the Current Year, Merchandise Is Sold for $86,000 Cash ...

Abbey Co Sold Merchandise to Gomez Co ...

Complete the Following Data Taken from the Condensed Income Statements ...